The Preliminary Ruling Procedure under Art. 267 TFEU

The preliminary ruling procedure according to Art. 267 TFEU (Treaty on the Functioning of the European Union) is a central instrument for ensuring the uniform application and interpretation of EU law within the member states. It plays a decisive role in the interaction between national law and the European legal framework. Especially in the context of financial courts, where tax law issues often have an international dimension, the preliminary ruling procedure is of great importance.

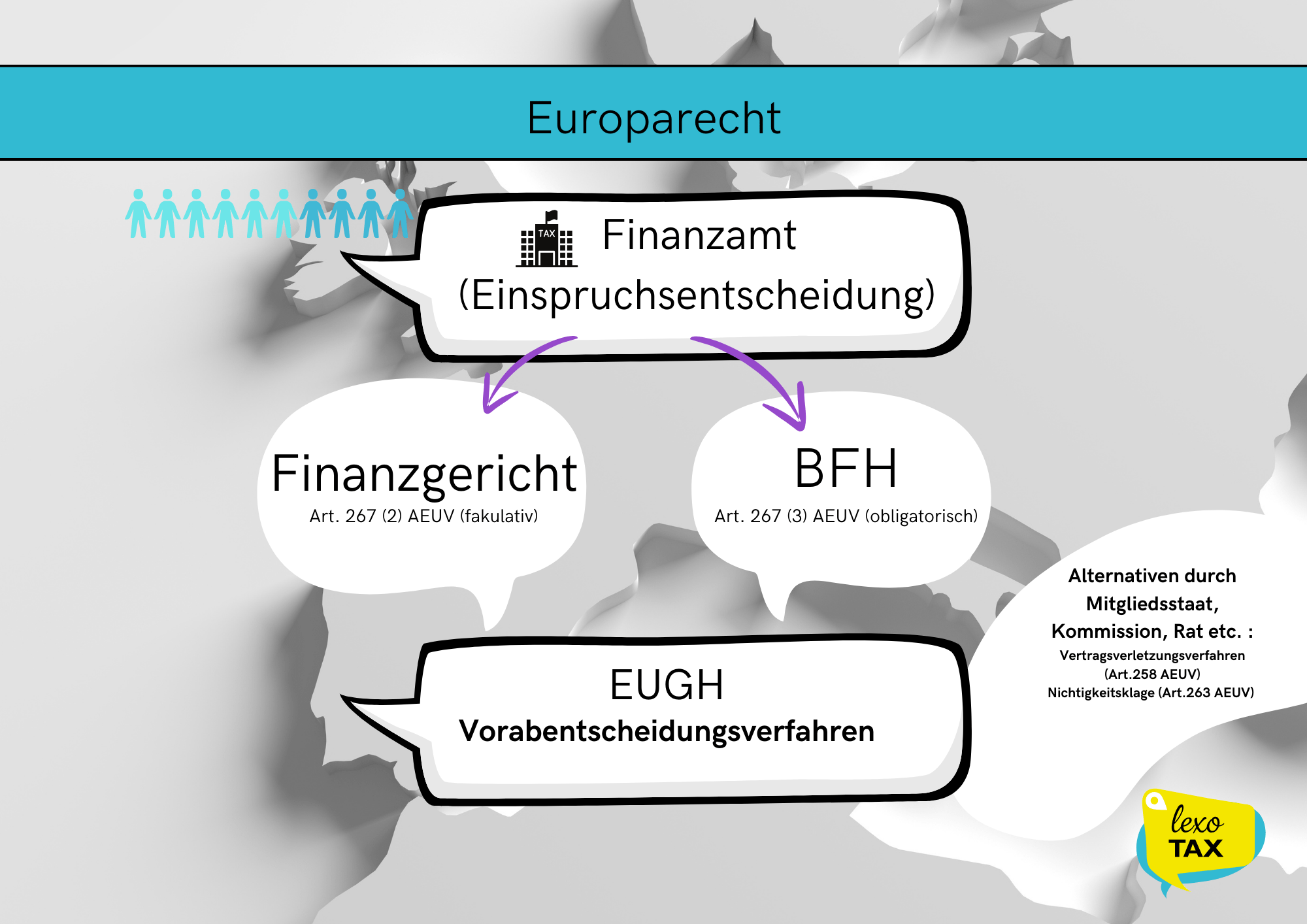

The Financial Court Procedure in Germany

The financial court procedure in Germany typically begins with an action against a tax assessment before the Finanzgericht (FG - Finance Court). The structure of this procedure provides for several instances, each taking on different roles in dealing with EU law issues.

- Court of First Instance: The Finanzgericht (FG) If an issue of European law arises during financial court proceedings that is relevant to the decision of the case, the Finanzgericht can decide to refer this question to the Court of Justice of the European Union (ECJ) for a preliminary ruling. This possibility arises from Art. 267 (2) TFEU, which allows courts to refer to the ECJ if they consider an interpretation of Union law necessary to decide the case.

- Court of Appeal: The Bundesfinanzhof (BFH) In contrast to the courts of first instance, which can make a referral to the ECJ at their own discretion, the Bundesfinanzhof (BFH - Federal Finance Court), as a court of last resort, is obliged under Art. 267 (3) TFEU to obtain a referral if a question of European law is decisive for the ruling. This applies unless there is clear case law from the ECJ on this issue (the so-called "acte clair" doctrine). This obligation ensures that Union law is applied uniformly in all member states and that no divergent national decisions arise that could counteract the goal of legal harmonisation.

Consolidated version of the Treaty on the Functioning of the European Union – PART SIX: INSTITUTIONAL AND FINANCIAL PROVISIONS – TITLE I: INSTITUTIONAL PROVISIONS – Chapter 1: The Institutions – Section 5: The Court of Justice of the European Union – Article 267 (ex Article 234 TEC)

_

Official Journal No. 115 of 09/05/2008 P. 0164 – 0164_

Article 267 (ex Article 234 TEC)

The Court of Justice of the European Union shall have jurisdiction to give preliminary rulings concerning:

a) the interpretation of the Treaties;

b) the validity and interpretation of acts of the institutions, bodies, offices or agencies of the Union;

Where such a question is raised before any court or tribunal of a Member State, that court or tribunal may, if it considers that a decision on the question is necessary to enable it to give judgment, request the Court to give a ruling thereon.

Where any such question is raised in a case pending before a court or tribunal of a Member State against whose decisions there is no judicial remedy under national law, that court or tribunal shall bring the matter before the Court.

If such a question is raised in a case pending before a court or tribunal of a Member State with regard to a person in custody, the Court of Justice of the European Union shall act with the minimum of delay.

The Preliminary Ruling Procedure under Art. 267 TFEU

The preliminary ruling procedure is a dialogue-based procedure between the national courts and the ECJ. It enables national courts to obtain a binding interpretation of Union law from the ECJ in cases of doubt.

- Course of the Procedure The national judge formulates one or more questions on the interpretation or validity of EU legal acts and transmits them to the ECJ. The latter examines the questions and issues a decision that exclusively concerns the interpretation or validity of EU law. The ECJ does not decide on the specific case itself, but provides the referring court with the necessary information on the interpretation of Union law so that the court can decide the case in accordance with EU law.

- Legal Effect of the ECJ Decision The ECJ's answer binds the referring court in the specific case and usually also has far-reaching effects on similar cases in other member states. The national court must make its decision based on the ECJ decision and interpret national law, as far as necessary, in the light of Union law.

- Obligation to Refer While lower courts (such as the FG) have the freedom under Art. 267 (2) TFEU to refer questions to the ECJ, courts of last resort (such as the BFH) are under an obligation to refer according to Art. 267 (3) TFEU. This obligation only lapses if the question has already been the subject of a previous ECJ decision or if the correct application of Union law is so obvious that no reasonable doubt can exist ("acte clair").

Preliminary Ruling Procedure

- The preliminary ruling procedure allows national courts to request an interpretation of EU legal provisions from the ECJ. This is particularly relevant when national courts are dealing with a case where it is unclear how a specific provision of EU law should be interpreted.

2. Interim Procedure between National Judiciary and ECJ

- Art. 267 TFEU creates an interim procedure in which national courts can ask the ECJ for advice before they deliver a judgment. Within this framework, the ECJ clarifies how EU law is to be interpreted, but leaves the application of this interpretation to the specific case to the national court.

3. Interpretation of EU Law by the ECJ

- The ECJ is tasked with interpreting EU law uniformly. This ensures that EU law is applied the same way in all member states and that no differences arise in the jurisprudence of individual countries.

4. Application to National Law by National Courts

- After the interpretation of EU law by the ECJ, national courts apply this interpretation to the specific case. They are obliged to follow the ECJ's specifications.

5. Legal Remedies and Obligation to Refer

- National courts that issue decisions against which no further legal remedies can be sought (such as the Bundesfinanzhof (BFH) in Germany) must submit a question on the interpretation of EU law to the ECJ if it is decisive for the outcome of the case. Other courts can do so, but are not obliged to.

6. Uniform Interpretation and Legal Certainty

- The preliminary ruling procedure contributes significantly to the uniform interpretation of EU law and promotes legal certainty in the EU. This is of particular importance to prevent EU law from being applied differently in various member states.

7. Relinquishment of Judicial Sovereignty and Primacy of EU Law

- By being obliged to adhere to the ECJ's interpretation, national courts give up a piece of their judicial sovereignty. This illustrates the primacy of EU law over national law and emphasizes the need for a coherent application of law throughout the Union.

8. Binding Effect and Retroactivity

- The ECJ's decisions in the preliminary ruling procedure have a binding effect on the national court that made the inquiry, as well as on other national courts in similar cases. Furthermore, the interpretation of EU law by the ECJ usually has retroactive effect, meaning that EU law is to be interpreted as if it had always applied in the manner determined by the ECJ.

Overall, Art. 267 TFEU contributes decisively to the consistency and uniformity of legal application in the EU by ensuring close cooperation between the national courts and the ECJ.

Special Cases and Current Developments

Since 1 October 2024, there has been a significant innovation in the preliminary ruling procedure

Jurisdiction for certain subject areas, such as the common system of value added tax and excise duties, has been partially transferred from the ECJ to the General Court of the European Union. This reform aims to reduce the workload of the ECJ and enable it to focus more on its role as the Union's constitutional court. At the same time, the General Court of the European Union is intended to handle the preliminary ruling questions transferred to it in these specific areas efficiently and while safeguarding the uniformity of Union law.

Important Changes:

- Transfer of Jurisdiction to the General Court of the European Union:

- Part of the jurisdiction for preliminary rulings is being transferred from the ECJ to the General Court of the European Union. This affects six specific subject areas, including the common system of value added tax and excise duties. This change is intended to reduce the ECJ's workload and allow it to focus more on more complex cases concerning the unity of Union law.

- Involvement of Further EU Institutions:

- In the future, all requests for a preliminary ruling will be notified to the European Parliament, the Council of the EU, and the European Central Bank. These institutions can then assess whether they have a particular interest in the questions raised and submit observations accordingly.

- Extended Publication Obligations:

- To improve transparency, the pleadings or written observations submitted by the parties in all preliminary ruling cases are to be published within a reasonable period after the conclusion of the case, provided the party does not object.

- Mechanism for Prior Admission of Appeals:

- The mechanism for the prior admission of appeals is being extended to further decisions of the General Court to ensure that the ECJ can focus on significant legal issues.

Based on the latest reforms in the European court system described in your document, the following jurisdictions arise for preliminary rulings within the framework of the ECJ and the General Court of the European Union:

Jurisdiction of the Court of Justice of the European Union (ECJ):

- Fundamental Questions of Union Law: The ECJ remains responsible for requests for preliminary rulings concerning the unity or coherence of Union law, particularly in complex or constitutional matters.

- Primary Law, International Law, and General Principles of Union Law: If a preliminary ruling touches upon questions of this nature, the ECJ also remains responsible.

- Cases with Mixed Questions: The ECJ retains jurisdiction if a request for a preliminary ruling concerns several areas, including those assigned to the General Court, but also involves other legal fields or fundamental questions.

Jurisdiction of the General Court of the European Union (from 1 October 2024):

- Common System of Value Added Tax: The General Court will be responsible for preliminary rulings that exclusively concern the EU's VAT system.

- Excise Duties: Likewise, the General Court will be responsible for preliminary ruling requests that relate only to excise duties.

- Customs Code and Tariff Classification of Goods: Preliminary rulings that relate exclusively to the Customs Code and the tariff classification of goods in the Combined Nomenclature fall under the jurisdiction of the General Court.

- Compensation and Assistance to Air and Rail Passengers: Questions relating to compensation claims for delays or cancellations of transport services will also be decided by the General Court.

- Greenhouse Gas Emission Allowance Trading System: The General Court will also be responsible for preliminary ruling requests in this area.

Important to Note:

- Examination by the ECJ: All requests for preliminary rulings will still be initially submitted to the ECJ. The ECJ then decides whether the request will be referred to the General Court if it falls exclusively into one of the subject areas mentioned above.

- Possibility of Referral: If a preliminary ruling within the General Court's jurisdiction raises a fundamental question, the General Court can refer it to the ECJ for a decision.

These changes take effect from 1 October 2024 and aim to reduce the workload of the ECJ while increasing the efficiency of the General Court of the European Union.

These reforms are part of a larger restructuring.

Procedure of the Preliminary Ruling Process

The procedure begins when a national court has a question about the interpretation or validity of EU law that is decisive for the ruling of a pending case. The national court can or must, depending on the instance, ask the ECJ for a preliminary ruling.

- Obligation and Discretion to Refer:

- Discretionary Referral (Art. 267 (2) TFEU): National courts can call upon the ECJ if they have doubts about the interpretation of Union law.

- Obligatory Referral (Art. 267 (3) TFEU): Courts whose decisions can no longer be challenged by legal remedies under national law (courts of last resort) are obliged to call upon the ECJ if a European law question arises that is decisive for the case.

- Decision of the ECJ:

- The ECJ examines the submitted question and provides an interpretation of Union law. This decision is binding for the national court. The ECJ makes no decision on the specific case itself, but interprets Union law or decides on its validity.

- Binding Effect and Legal Consequences:

- The ECJ's decision binds the referring court and often also has effects on similar cases in other member states. The ECJ's interpretation is authoritative for all courts that have to deal with the same question.

Landmark Rulings

The Schumacker Case (C-279/93)

Facts of the Case:

Mr Schumacker, a Belgian citizen, worked in Germany and earned the majority of his income there but lived in Belgium. Germany taxed his income as a person with limited tax liability (because he was not resident in Germany) but did not grant him certain tax benefits granted to taxpayers resident in Germany. These benefits, such as the basic tax-free allowance and spouse splitting, were denied to him on the grounds that he was not resident in Germany.

Mr Schumacker filed a lawsuit against this, arguing that this treatment was discriminatory since he earned the majority of his income in Germany and should therefore be treated for tax purposes the same as an employee resident in Germany.

Procedural Course:

- Action before the Finanzgericht:

- Mr Schumacker brought an action before a German Finanzgericht against the decision of the German tax authorities to deny him the tax benefits granted to domestic taxpayers. He claimed this was a violation of the principle of equal treatment and the freedom of movement for workers within the EU.

- Referral to the ECJ (Art. 267 TFEU):

- The German Finanzgericht referred the question to the ECJ whether the refusal to grant a non-resident worker the same tax benefits as a resident worker was compatible with the provisions of the EC Treaty (now TFEU) on the freedom of movement for workers.

- Decision of the ECJ:

- The ECJ ruled that in a situation like Mr Schumacker's, where the non-resident worker earns almost all his income in the state where he works, it is discriminatory not to grant him the same tax benefits as a resident taxpayer. The ECJ found that there is no objective reason for the unequal treatment of resident and non-resident taxpayers if both are in the same situation, particularly if the non-resident taxpayer has no significant income in the state of residence that could be taxed there.

- Consequences for the National Procedure:

- The German Finanzgericht had to adapt the German income tax regulations in light of the ECJ's decision. As a result, Mr Schumacker received the same tax benefits as an employee resident in Germany.

Significance of the Case:

The Schumacker case was a milestone in the development of EU law in the field of direct taxation. It clarified that when taxing workers who work in another member state, member states must ensure they are not discriminated against, especially if they earn all or almost all of their income in the working state. The case led to many EU member states having to adapt their tax regulations to avoid discrimination based on residence and to ensure the freedom of movement for workers.

This case is particularly relevant for income tax and shows how the preliminary ruling procedure helps to ensure compliance with the fundamental freedoms of the EU even in the area of direct taxation.

The Danner Case (C-136/00)

Facts of the Case:

Mr Danner, a taxpayer resident in Germany, paid contributions to a private pension insurance scheme taken out with an insurance company in Finland. The German tax office refused the deduction of these contributions as special expenses (Sonderausgaben) because they were paid to an insurer outside Germany. Under German tax law, only contributions to domestic insurers were deductible.

Danner then filed an action at the Finanzgericht. He argued that this regulation violated the freedom to provide services (Art. 56 TFEU) anchored in the EU treaties, as it represented discrimination based on the seat of the service provider.

Procedural Course:

- Action before the Finanzgericht:

- The Finanzgericht Hamburg, which was dealing with the case, recognized that the question of the deductibility of contributions was directly related to the interpretation of EU law. In particular, it concerned whether German tax law was compatible with the freedom to provide services.

- Referral to the ECJ (Art. 267 TFEU):

- The Finanzgericht decided to refer the question to the ECJ for a preliminary ruling. It asked whether it violates the freedom to provide services if a member state refuses the deduction of insurance contributions paid to an insurer in another member state.

- Decision of the ECJ:

- The ECJ ruled that the German regulation indeed constitutes a restriction on the freedom to provide services, as it makes insurance services provided by providers in other member states unattractive. Such restrictions can, however, be justified if they are based on overriding reasons of public interest and are proportionate.

- In this case, while the ECJ recognized that the coherence of the tax system can be a legitimate goal, it found that the German regulation was not proportionate and therefore violated the freedom to provide services.

- Consequences for the National Procedure:

- After the ECJ decision, the case returned to the Finanzgericht Hamburg, which had to interpret the national provisions in light of the ECJ ruling. Ultimately, the German regulation was seen as incompatible with EU law, and Mr Danner was able to claim the deduction of the insurance contributions.

Significance of the Case:

The Danner case was significant because it showed the limits of national tax sovereignty in relation to the freedom to provide services. It demonstrated that national tax rules that represent discrimination against service providers resident abroad can collide with EU law. The case also led to an adjustment of German tax laws to bring the regulations into line with EU law.

The Marks & Spencer Case (C-446/03)

Facts of the Case:

Marks & Spencer, a British retail company, earned profits in Great Britain and maintained subsidiaries in other EU member states, including Belgium, France, and Germany. These subsidiaries generated losses. Under British tax law, losses generated by subsidiaries in other countries could not be offset against the profits of the parent company in the home country.

Marks & Spencer filed a lawsuit and argued that the refusal of cross-border loss offsetting violated the freedom of establishment under Art. 49 TFEU and the freedom of capital movement under Art. 63 TFEU.

Procedural Course:

- Action before British Courts:

- The case was initially heard before a British court. The court saw the need to ask the ECJ for an interpretation of the relevant EU legal provisions, particularly regarding the question of whether the ban on cross-border loss offsetting violates EU fundamental freedoms.

- Referral to the ECJ (Art. 267 TFEU):

- The British court referred the question to the ECJ for a preliminary ruling. It wanted to know whether the refusal of loss offsetting for foreign subsidiaries was compatible with EU fundamental freedoms.

- Decision of the ECJ:

- The ECJ ruled that the ban on cross-border loss offsetting fundamentally constitutes a restriction on the freedom of establishment. However, the ECJ stated that such restrictions could be justified under certain circumstances.

- The ECJ formulated the "final losses" doctrine: If a subsidiary abroad definitively has no further possibility of asserting its losses for tax purposes in its own member state (e.g., because the subsidiary is liquidated), the parent company must be allowed to offset these losses in the home country.

- Consequences for the National Procedure:

- Following the ECJ decision, the British court had to decide whether the losses generated in the foreign subsidiaries of Marks & Spencer were to be regarded as "final losses" that could be offset in Great Britain. Ultimately, it was determined that the losses of the foreign subsidiaries in this specific case were indeed to be regarded as "final," and Marks & Spencer was allowed to claim these losses for tax purposes in Great Britain.

Significance of the Case:

The Marks & Spencer case had far-reaching effects on the tax treatment of cross-border corporate structures within the EU. It clarified that the freedom of establishment fundamentally also includes the right to cross-border loss offsetting as long as certain conditions are met. This judgment forced several EU member states to adapt their national tax regulations to safeguard EU fundamental freedoms, and it led to an intensive debate about the limits of the tax autonomy of member states within the EU.

The Cadbury Schweppes Case (C-196/04)

Facts of the Case:

Cadbury Schweppes, a British group, founded two subsidiaries in Ireland where the tax burden was lower than in the United Kingdom. The British tax authorities applied the British CFC rules to these subsidiaries, which served to tax income from foreign subsidiaries in low-tax countries as if they had arisen in Great Britain. Cadbury Schweppes argued that this application of the CFC rules violated the freedom of establishment according to Art. 49 TFEU.

Excursus: Controlled Foreign Company (CFC) rules are tax provisions aimed at preventing the shifting of income into subsidiaries in low-tax countries. These rules are used by many countries to ensure that profits earned in so-called Controlled Foreign Companies (foreign subsidiaries controlled by domestic companies) do not remain untaxed or only lightly taxed.

Procedural Course:

- Action before British Courts:

- Cadbury Schweppes brought an action against the application of the CFC rules, stating that they represent an unjustified restriction on the freedom of establishment since they hinder the establishment and operation of subsidiaries in other member states of the EU.

- Referral to the ECJ (Art. 267 TFEU):

- The British court saw the question as decisive for the ruling and referred the question to the ECJ whether the application of the CFC rules in the case of Cadbury Schweppes' subsidiaries in Ireland violated the freedom of establishment.

- Decision of the ECJ:

- The ECJ found that CFC rules fundamentally constitute a restriction on the freedom of establishment, as they could deter companies from founding subsidiaries in other member states. Such a restriction can, however, be justified if it is necessary to avoid tax evasion.

- The ECJ ruled that CFC rules may only be applied if they specifically aim to prevent artificial arrangements that serve exclusively to obtain tax advantages. In the case of Cadbury Schweppes, the ECJ found that the Irish subsidiaries actually carried out economic activities and therefore could not be regarded as purely artificial arrangements.

- Consequences for the National Procedure:

- Following the ECJ decision, the British court had to examine whether the subsidiaries of Cadbury Schweppes in Ireland conducted genuine economic activities. Since this was the case, the company was able to claim the freedom of establishment, and the CFC rules could not be applied.

Significance of the Case:

The Cadbury Schweppes case had significant impact on national tax regulations in the EU. It limited the application of CFC rules and clarified that such regulations are only compatible with EU law if they are specifically directed against artificial arrangements that serve exclusively to achieve tax advantages. The judgment emphasized the need for a balance between combating tax avoidance and protecting the freedom of establishment.

This judgment led to many EU member states having to adapt their CFC rules to ensure they are compatible with EU law. It also underscored the importance of the preliminary ruling procedure under Art. 267 TFEU as a means of clarifying questions concerning the balance between national tax policy and the fundamental freedoms of the internal market.

The preliminary ruling procedure helps ensure the uniformity of EU law and adapts national regulations to the requirements of the internal market. Particularly in the area of tax law, this reform will change the way certain tax law preliminary rulings are handled, which could be significant for taxpayers throughout the EU.

The preliminary ruling procedure according to Art. 267 TFEU is an indispensable element of the European legal system. It secures the uniform interpretation and application of Union law and promotes cooperation between national courts and the ECJ. Through this procedure, it is guaranteed that EU law is applied coherently in all member states, which contributes to the stability and predictability of the European internal market. The recent reforms to transfer jurisdictions to the General Court of the European Union show that this procedure remains of central importance for the functionality of the EU legal order.

**

Note

**This article is for general information purposes and was carefully created by the Lexo.Tax editorial team. Personal tax advice can only be provided within the context of membership in lexo.tax – and exclusively to the legally permissible extent according to § 4 Nr. 11 StBerG (Tax Consultancy Act).