"Transfer pricing is the focal point of tax audits and therefore entails significant risks."

Basics of Transfer Pricing Documentation

Transfer prices are the prices that companies within a group agree upon for the transfer of goods, services, or intangible assets between related parties. These prices must comply with the arm's length principle, meaning they must be structured in the same way as they would be agreed between independent third parties. Transfer pricing documentation serves to prove this appropriateness and to fulfill the requirements of tax regulations.

Legal Basis

The most important legal bases for transfer pricing documentation in Germany include:

- § 1 Außensteuergesetz (AStG - Foreign Tax Act): Regulates the correction of income in international contexts if the transfer prices do not comply with the arm's length principle.

- § 90 Abs. 3 Abgabenordnung (AO - Fiscal Code): Obliges taxpayers to prepare documentation proving the appropriateness of transfer prices (Local File and Master File).

- § 162 AO: Authorises the tax authorities to estimate tax bases if no documentation or unusable documentation is submitted.

- § 162 Abs. 4 AO: Regulates penalty surcharges in cases of delayed, incomplete, or unusable documentation.

- Gewinnabgrenzungsaufzeichnungsverordnung (GAufzV - Profit Allocation Record-Keeping Ordinance): Provides detailed requirements for transfer pricing documentation.

Transfer Pricing Methods

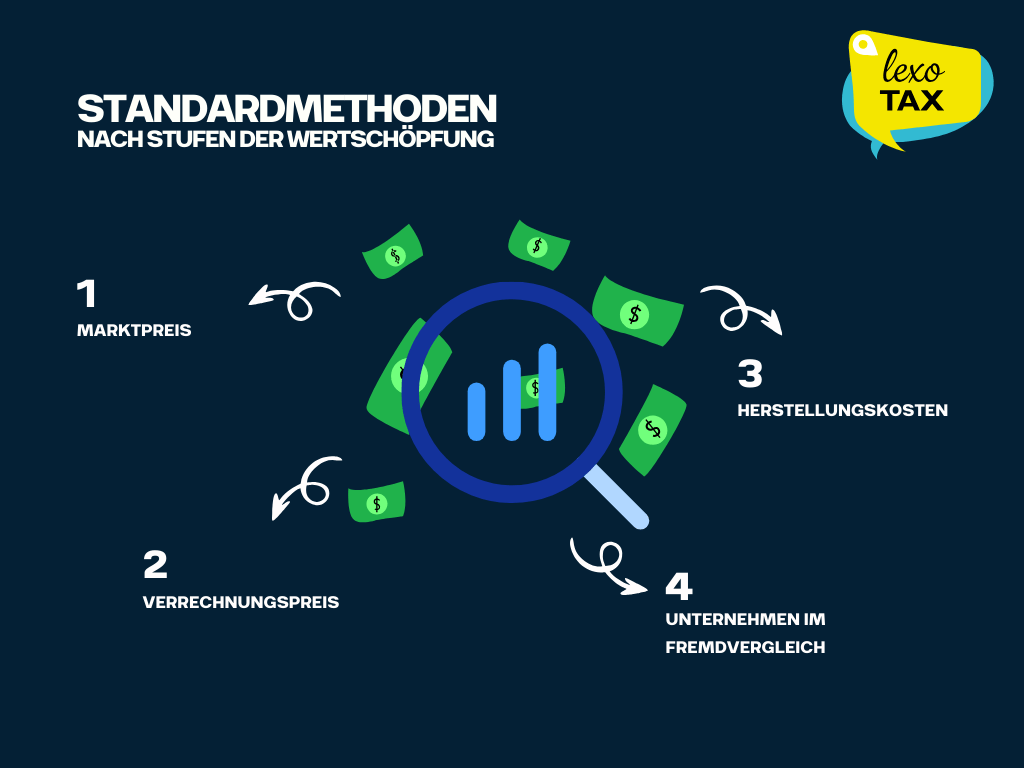

The documentation must make the applied transfer pricing methods transparent. The common methods are:

- Comparable Uncontrolled Price Method (CUP): Comparison of prices between related companies and independent third parties.

- Resale Price Method: Derivation of the transfer price from the resale price minus an appropriate margin.

- Cost Plus Method: Calculation of the transfer price as the sum of costs and an appropriate profit mark-up.

- Profit-Oriented Methods: Such as the Transactional Net Margin Method (TNMM), which uses net profit as the basis for the arm's length comparison.

Documentation Obligations and Legal Consequences

Companies must maintain detailed records that justify their transfer prices and prove compliance with legal requirements. If a company fails to meet these obligations or provides insufficient documentation, it faces severe sanctions, such as income corrections and penalty surcharges.

Applying the Theory to Case Examples

Worst-Case Scenario:

Fact Pattern:

M-AG (Germany) sells model cars to its US subsidiary Car-Inc. for €500,000. The tax audit determines an arm's length price range for the model cars between €550,000 and €650,000. The transfer pricing documentation submitted by M-AG is classified as unusable by the tax audit.

Application of Sections and Detailed Calculation:

- § 8 Abs. 1 Körperschaftsteuergesetz (KStG - Corporate Income Tax Act):

- Principle: According to § 8 Abs. 1 KStG, income to be determined in accordance with the German Income Tax Act (EStG) is subject to corporate income tax. This means that all components of income recorded as part of the tax profit determination flow into the assessment basis for corporate income tax.

- Application in the case: M-AG set the transfer price too low (€500,000 instead of the arm's length value). This leads to an income correction.

- Valuation at Going-Concern Value according to § 6 Abs. 1 Nr. 5 Satz 1 Einkommensteuergesetz (EStG - Income Tax Act):

- Principle: § 6 Abs. 1 Nr. 5 Satz 1 EStG stipulates that in the case of the transfer of assets to related companies that does not occur at an arm's length price, the difference must be corrected to the "Teilwert" (going-concern value). The going-concern value is the amount that a purchaser would allocate to an individual asset as part of the purchase of the entire company.

- Application in the case: Here, it is assumed that the going-concern value of the model cars is €550,000 (the lower end of the arm's length range). Thus, the actual transfer price of €500,000 is below the going-concern value.

- § 1 Abs. 3 Außensteuergesetz (AStG) – Arm's Length Principle:

- Principle: If transfer prices between related companies do not comply with the arm's length principle, an income correction must be made. According to § 1 Abs. 3 AStG, the correction is made to the median value, provided the actual transfer price does not comply with the arm's length principle.

- Application in the case: Since the established arm's length price range lies between €550,000 and €650,000 and the set price of €500,000 is below this, a correction is made. As the documentation is classified as unusable, the tax authorities can make the correction at the upper end of the range according to § 162 Abs. 3 AO (see below), i.e., to €650,000.

- § 162 Abs. 3 Abgabenordnung (AO) – Estimation Power:

- Principle: Tax authorities may estimate the tax bases if no usable records are submitted. This estimation may be oriented towards the upper end of the arm's length range.

- Application in the case: The tax administration estimates the arm's length price at €650,000, as the submitted documentation is unusable. This results in an increase in taxable income of €150,000 (€650,000 – €500,000).

- Penalty Surcharge according to § 162 Abs. 4 Abgabenordnung (AO):

- Principle: § 162 Abs. 4 AO allows for the imposition of penalty surcharges of at least €5,000 or 5% to 10% of the additional amount of estimated income if documentation is delayed, incomplete, or unusable.

- Application in the case: The difference amount is €150,000, and the penalty surcharge is set at 10% of the difference. This results in a penalty surcharge of €15,000 (10% of €150,000).

- § 4 Abs. 5 Nr. 12 Einkommensteuergesetz (EStG) – Non-deductible Business Expenses:

- Principle: § 4 Abs. 5 Nr. 12 EStG stipulates that fines, administrative penalties, and similar punitive payments made to authorities are not deductible as business expenses.

- Application in the case: The penalty surcharge of €15,000 according to § 162 Abs. 4 AO counts as a non-deductible business expense. This means that this amount may not be deducted when determining the tax assessment basis, further increasing M-AG's tax burden.

Summary of the Additional Burden:

- Income Correction:

- Increase in income according to § 8 Abs. 1 KStG (constructive dividend - vE);

- Valuation at going-concern value (§ 6 Abs. 1 Nr. 5 S. EStG): +€50,000

- To the extent § 1 AStG is fulfilled; correction to median (§ 1 Abs. 3 S. 4 AStG): +€50,000

- Since documentation is unusable, correction possible up to the upper end of the range (§ 162 Abs. 4 S. 2 AO): +€50,000

- Increase in income by €150,000 due to estimation by the tax administration at the upper end of the range (€650,000).

- Additional Tax Burden:

- Additional Tax: €150,000 x 30% = €45,000

- At an assumed tax rate of 30% (including corporate income tax, solidarity surcharge, and trade tax), this results in an additional tax burden of €45,000 (€150,000 x 30%).

- Penalty Surcharge:

- Penalty surcharge according to § 162 Abs. 4 S. 2 AO in the amount of 10% of €150,000: +€15,000 (> €5,000)

- Penalty surcharge is a non-deductible business expense (§ 4 Abs. 5 Nr. 12 EStG)

- The penalty surcharge is €15,000 (10% of the €150,000 difference) according to § 162 Abs. 4 AO. It would also be justifiable to apply the penalty surcharge only to the correction according to § 162 Abs. 3 AO. This penalty surcharge is not deductible as a business expense according to § 4 Abs. 5 Nr. 12 EStG.

Total additional burden: €60,000 (€45,000 additional tax burden + €15,000 penalty surcharge).

M-AG's financial burden thus consists of the additional tax burden due to the income correction and the non-deductible penalty surcharge. This underlines the grave consequences that unusable transfer pricing documentation can entail.

Best-Case Scenario:

Fact Pattern:

M-AG (Germany) sells model cars to its US subsidiary Car-Inc. for €500,000. The tax audit determines an arm's length range for the model cars between €550,000 and €650,000. The transfer pricing documentation submitted by M-AG is initially considered insufficient. However, during further research, M-AG finds a substantiated arm's length price of €500,000, which it can submit retrospectively.

Application of Sections and Detailed Calculation:

- § 1 Abs. 3 Außensteuergesetz (AStG) – Arm's Length Principle:

- Principle: According to § 1 Abs. 3 AStG, income between related companies must be determined as it would have been agreed between independent third parties (arm's length principle). If the price actually agreed does not correspond to the arm's length principle, a correction must be made.

- Application in the case: In the best case, M-AG succeeds in substantiating an arm's length price of €500,000 that complies with the arm's length principle. This eliminates the need for an income correction. The tax audit accepts the proven price as arm's length, and the original agreement remains unchanged.

- § 162 Abs. 3 Abgabenordnung (AO) – Estimation Power:

- Principle: § 162 Abs. 3 AO enables tax authorities to estimate tax bases if no usable records are submitted. This estimation can be oriented at the upper end of the arm's length range.

- Application in the case: Since M-AG can retrospectively provide substantiated proof of the arm's length price of €500,000, the tax authorities' power to estimate is waived. An estimation of income at the upper end of the range (€650,000) is not required.

- § 8 Abs. 1 Körperschaftsteuergesetz (KStG) – Tax Assessment Basis:

- Principle: According to § 8 Abs. 1 KStG, income to be determined in accordance with the German Income Tax Act (EStG) is subject to corporate income tax.

- Application in the case: Since no correction of transfer prices is necessary, the assessment basis for corporate income tax remains unchanged at €500,000. No additional tax burden arises.

- Possible Late Surcharge according to § 162 Abs. 4 Abgabenordnung (AO):

- Principle: If documentation is delayed, incomplete, or unusable, penalty surcharges of at least €5,000 or 5% to 10% of the additional amount of estimated income can be imposed according to § 162 Abs. 4 AO.

- Application in the case: Since M-AG can retrospectively explain the arm's length price in a substantiated manner, the tax administration might consider a late surcharge. However, this would only be imposed if the subsequent delivery of documentation is rated as delayed. In this case, a minimal late surcharge in the amount of €5,000 could be levied, depending on the tax administration's assessment of the circumstances.

- § 4 Abs. 5 Nr. 12 Einkommensteuergesetz (EStG) – Non-deductible Business Expenses:

- Principle: § 4 Abs. 5 Nr. 12 EStG stipulates that fines, administrative penalties, and similar punitive payments made to authorities are not deductible as business expenses.

- Application in the case: If a late surcharge according to § 162 Abs. 4 AO were imposed, it would not be deductible as a business expense. If the late surcharge is, for example, €5,000, this amount cannot be claimed to reduce tax.

Summary of the Burden in the Best Case:

- No Income Correction:

- Since the arm's length price of €500,000 can be substantiated (transfer price is at arm's length), no correction of income to €650,000 occurs according to § 8 Abs. 1 KStG in conjunction with § 162 Abs. 3 AO. No additional taxable income arises.

- No Additional Tax Burden:

- Since the income is not corrected, the tax burden remains unchanged. No additional tax arises.

- Possible Late Surcharge:

- If the subsequent delivery of the arm's length price is considered delayed, a minimal late surcharge according to § 162 Abs. 4 S. 3 AO of €5,000 could be imposed. This amount would not be deductible as a business expense according to § 4 Abs. 5 Nr. 12 EStG.

Total burden in the best case: €0 to €5,000, depending on whether a late surcharge is imposed.

Conclusion:

In the best-case scenario, no additional tax burdens arise for M-AG, as the retrospectively proven arm's length price of €500,000 is recognised. The only possible burden would be a late surcharge of €5,000 if the tax administration views the subsequent submission of documentation as delayed. This late surcharge would not be deductible as a business expense.

These scenarios show how important it is to quickly provide subsequent evidence in case of doubts regarding transfer pricing documentation to minimise potential tax risks.

Suitable Transfer Pricing Method

Fact Pattern:

A domestic production plant (M-AG) in the clothing industry supplies its foreign sales subsidiary (Car-Inc.) with products. The transfer price is calculated by the production plant using the Cost Plus Method. However, the sales subsidiary makes very high profits. Furthermore, the expenses for market development abroad were borne by the German parent company.

Problem Definition:

The Cost Plus Method applied by the production plant results in the sales subsidiary (Car-Inc.) achieving very high profits due to the high sales prices. However, since the sales subsidiary is a routine company whose function and risk are lower, this method appears unsuitable as it leads to an unequal distribution of profits.

Application of Sections and Detailed Analysis:

- § 1 Abs. 1 Außensteuergesetz (AStG) – Arm's Length Principle:

- Principle: § 1 Abs. 1 AStG requires that transfer prices between related companies must correspond to what would have been agreed between independent third parties under comparable conditions. This is the so-called arm's length principle.

- Application in the case: In this case, it must be checked whether the applied Cost Plus Method actually fulfills the arm's length principle. Since the sales subsidiary only performs routine functions and bears lower risks, it does not seem appropriate for it to receive all market development profits. An arm's length comparison would likely project a different profit distribution between the parent and subsidiary company.

- Cost Plus Method – § 1 Abs. 3 AStG:

- Principle: Under the Cost Plus Method, the transfer price is calculated as the sum of the costs incurred and an appropriate profit mark-up. This method is particularly suitable for routine functions and standardised services or production.

- Application in the case: The Cost Plus Method in this case leads to the sales subsidiary achieving very high profits, while the parent company, which bears the market development costs, only receives low profits. Since the sales subsidiary is to be regarded as a routine company, it should only achieve a stable but low profit. This method is therefore unsuitable in this case.

- Resale Price Method – Alternative Method:

- Principle: The Resale Price Method is particularly suitable for distribution companies that do not assume significant functions or risks. In this method, the transfer price is calculated from the resale price of the goods minus an appropriate margin that corresponds to the distribution functions and risks of the company.

- Application in the case: Since the sales subsidiary only performs routine functions and the market development costs were borne by the parent company, the Resale Price Method is the more suitable method. This method would ensure that the sales subsidiary only receives an appropriate margin on its sales prices, while the residual profit is allocated to the parent company, which bears the essential functions and risks.

- § 1 Abs. 3 Satz 4 AStG – Income Correction:

- Principle: If the chosen transfer pricing method does not comply with the arm's length principle, an income correction can be made. This is done to determine the income as it would have arisen between independent third parties.

- Application in the case: Since the Cost Plus Method is not suitable, the tax administration could correct the income of the sales subsidiary and shift the profit to the parent company. This correction would follow the Resale Price Method, whereby the sales subsidiary would achieve a lower margin and the parent company a higher profit.

Summary:

- Unsuitable Method – Cost Plus Method:

- The application of the Cost Plus Method leads to an unequal and inappropriate profit distribution, where the sales subsidiary achieves high profits despite only fulfilling routine functions. This method is therefore unsuitable in this case.

- Suitable Method – Resale Price Method:

- The Resale Price Method is better suited for distribution companies with routine functions. It ensures that the sales subsidiary only receives an appropriate margin on its sales prices, while the main profit is allocated to the parent company, which bears the essential functions and risks.

- Correction of Income:

- If the originally applied method does not comply with the arm's length principle, a correction of income can be made. This correction would increase the income of the parent company and reduce that of the sales subsidiary accordingly to ensure a fair profit distribution.

Conclusion: In this case, it is evident that the choice of transfer pricing method is crucial for an appropriate profit distribution between the parent and subsidiary company. While the Cost Plus Method leads to an incorrect distribution, the Resale Price Method offers a more appropriate solution that better complies with the arm's length principle.

An incorrect choice of method can lead to significant tax risks and income corrections.

Data Screening to Determine the Transfer Price

Fact Pattern:

A domestic subsidiary (M-AG) receives goods from its foreign parent company, which are sold on the German market with a return on sales of 1%. The transfer price is determined through data screening (Transactional Net Margin Method, TNMM) at other distribution companies. A range of 1% to 7.5% is used. This range results from the values of approximately 20 comparable companies operating exclusively in Eastern Europe. The first quartile of the range is 3%, the third quartile is 6%, and the median is 4%.

Problem Definition:

The tax administration must decide whether the range used to determine the transfer price of the domestic subsidiary is appropriate, especially given that the comparable companies operate in Eastern Europe while the domestic subsidiary acts in the German market.

Application of Sections and Detailed Analysis:

- § 1 Abs. 1 Außensteuergesetz (AStG) – Arm's Length Principle:

- Principle: The arm's length principle according to § 1 Abs. 1 AStG requires that transfer prices between related companies be set as they would have been agreed between independent third parties under comparable conditions.

- Application in the case: The determined range (1% to 7.5%) is based on comparable companies operating exclusively in Eastern Europe. As there may be differences in market conditions between Eastern Europe and Germany, it must be checked whether this range actually represents an appropriate arm's length comparison.

- Transactional Net Margin Method (TNMM) – § 1 Abs. 3 AStG:

- Principle: The TNMM is a method for determining the transfer price where the net margin of a controlled transaction (e.g., between related companies) is compared with the net margin of a comparable uncontrolled transaction.

- Application in the case: When applying the TNMM to the domestic subsidiary, a range of 1% to 7.5% was set. The median of this range is 4%. This method is generally permissible; however, the comparability of the data must be critically questioned.

- Limitation of the Range due to Restricted Comparability – § 1 Abs. 3 Satz 2 AStG and Paragraph 53 VWG 2020:

- Principle: If the comparability of the data used is restricted, for example because the comparable companies operate in different markets, the range can be narrowed. This means the tax administration applies the range only in the sub-area that is most comparable. Paragraph 53 of the Administrative Principles for Transfer Pricing 2020 (VWG 2020) emphasises the need to critically examine the comparability of data and, if necessary, adjust the range.

- "Since results from a pure database screening are regularly insufficient for checking the comparability of circumstances and thus the appropriateness documentation, supplementary search steps and selection procedures must be recorded and documented accordingly (cf. § 4 Para. 3 GAufzV). The data created and compiled by the taxpayer for this purpose must be made accessible to the tax authority in electronic form within the scope of § 147 Para. 5 and 6 AO."

- Application in the case: Due to geographical differences and potentially different market conditions between the Eastern European comparable companies and the domestic subsidiary, the tax administration could narrow the range from 1% to 7.5%. For example, the range could be narrowed to the first to third quartile (3% to 6%) to ensure better comparability. Paragraph 53 VWG 2020 stresses the importance of a careful analysis of comparability to avoid distortions.

- BFH Ruling of 17 October 2001, I R 103/00, IStR 2001, p. 745:

- Principle: In this ruling, the Bundesfinanzhof (BFH) clarified that when applying the TNMM, the comparability of the data used must be examined with particular care. If the comparable companies operate in other markets, differences in market conditions must be taken into account and the range adjusted accordingly.

- Application in the case: The BFH ruling supports the need to critically question the comparable data used and to adjust the range if necessary. In the present case, this could mean that the originally set range of 1% to 7.5% is adjusted to account for the different market conditions between Eastern Europe and Germany.

- Correction to the Median Value – § 1 Abs. 3 Satz 4 AStG:

- Principle: Once a range has been narrowed, a correction to the median value of this range can be made to ensure that the transfer price complies with the arm's length principle.

- Application in the case: After narrowing the range (e.g., to 3% to 6%), the tax administration could perform a correction of the transfer price to the median value of the narrowed range, i.e., to 4%. This would mean that the return on sales of the domestic subsidiary is adjusted to 4% if the original value was only at 1%.

- § 162 Abs. 3 Abgabenordnung (AO) – Estimation:

- Principle: If no usable documentation is provided or the submitted documentation is considered insufficient, the tax authorities can estimate the tax bases. This estimation could also be based on the narrowed and corrected values.

- Application in the case: Should the submitted documentation be considered insufficient, the tax authorities could perform an estimation based on the corrected median value of 4% to correct the transfer price of the domestic subsidiary.

Summary:

- Application of the TNMM:

- The TNMM is generally suitable for determining the transfer price of the domestic subsidiary. However, the comparability of the data used must be critically examined, especially if the comparable companies operate in a different market (Eastern Europe).

- Narrowing the Range according to Paragraph 53 VWG 2020 and BFH Ruling:

- Due to restricted comparability, the tax administration can narrow the original range of 1% to 7.5% to a narrower range, e.g., 3% to 6%, to improve comparability. This approach is supported by both Paragraph 53 VWG 2020 and the BFH ruling of 17 October 2001.

- Correction to the Median Value:

- After narrowing the range, the transfer price can be corrected to the median value of this range (4%) to fulfill the arm's length principle.

- Estimation of Tax Bases:

- If the submitted documentation is not sufficient, the tax authorities could estimate the transfer price based on the corrected median value of 4%.

Conclusion: In the case of data screening, it is shown that the choice of comparable companies and the determination of the range are crucial for the appropriateness of the transfer price. An uncritical adoption of comparison data from other markets can lead to an inappropriate range and thus to faulty transfer prices. By narrowing the range and correcting to the median value, it can be ensured that the transfer price meets the requirements of the arm's length principle. The application of Paragraph 53 VWG 2020 and the consideration of the BFH ruling of 17 October 2001 strengthen the necessity for a careful examination and adjustment of comparable data.

EXCURSUS: The ruling of the Bundesfinanzhof (BFH) of 18 May 2021 (I R 4/17) deals with the determination of arm's length loan interest rates in the context of transfer pricing within a group.

Core Points of the Ruling:

- Primacy of the CUP Method:

- The BFH emphasises that before applying the Cost Plus Method, it must be checked whether the Comparable Uncontrolled Price (CUP) method can be applied to determine the arm's length interest rates. This applies in particular to unsecured group loans, regardless of whether they were granted by the parent company or an intra-group financing company.

- "Stand-alone" Rating:

- For the assessment of creditworthiness, the credit standing of the individual borrowing group company is decisive, not the average creditworthiness of the overall group. Internal group support can only be considered if it is strengthened by legally binding commitments and an external lender would recognise this as creditworthiness-enhancing.

- Criticism of the Lower Court's Estimation Method:

- The Münster Finance Court had applied the Cost Plus Method without sufficient checking as to whether the CUP method would have been applicable. This approach was considered insufficient by the BFH, as the CUP method should generally be preferred if corresponding comparison values are available.

- Dismissal and Remand:

- The ruling of the Münster Finance Court was overturned, and the case was remanded to the Finance Court for a new hearing and decision. The Finance Court must now examine more closely whether the CUP method can be applied and whether the applied "stand-alone" rating was correct.

Conclusion:

The ruling emphasises the importance of the CUP method in determining transfer prices and the need to assess the creditworthiness of individual group companies independently of the overall group. It clarifies that a flat application of the Cost Plus Method is not permissible if a more direct and precise method (such as the CUP method) is available.

Currently, it remains to be seen whether the tax administration will adjust its position or whether a non-application decree (Nichtanwendungserlass) might be issued, which would mean that the BFH ruling only applies to the specific individual case and cannot be transferred to other cases. Nevertheless, companies should be attentive and disclose potential deviations between the BFH decision and official administrative practice in their tax returns to minimise risks in later tax audits.

Chargeable Services and Deductibility

Fact Pattern:

A German subsidiary (M-AG) receives services from its foreign parent company in the field of financing advice. For this, M-AG pays a fee to the parent company. The question is whether this payment is recognised as a chargeable service and can be tax-deductible as a business expense.

Problem Definition:

The central question is whether the fee that the German subsidiary pays to the parent company is rendered for a service that is in the interest of the subsidiary and thus constitutes a chargeable service. Furthermore, it must be checked whether the payment constitutes deductible business expenses or whether they are classified as "shareholder expenses", which are not deductible.

Application of Sections and Detailed Analysis:

- § 4 Abs. 4 Einkommensteuergesetz (EStG) – Business Expenses:

- Principle: According to § 4 Abs. 4 EStG, business expenses are those expenditures caused by the business operations. These expenses are generally tax-deductible if they are professionally induced and serve the business.

- Application in the case: The fee that the German subsidiary pays to the parent company for financing advice is deductible as a business expense if it is caused by the business and the advice is based on a business necessity. The advice must occur in the interest of the German subsidiary and not just in the interest of the overall corporate group (in the sense of the shareholder).

- § 1 Außensteuergesetz (AStG) – Arm's Length Principle:

- Principle: § 1 AStG requires that services between related companies be rendered and remunerated at arm's length conditions. This means that the remuneration for the financing advice must correspond to what independent third parties would agree under the same conditions.

- Application in the case: To check the arm's length nature of the fee, various approaches can be used:

- External Fees (CUP Method): A comparison with the fees that independent consulting firms charge for similar services can serve as a basis. For example, hourly rates or flat fees from external consulting firms can be used to check whether the fee charged by the parent company is customary in the market.

- Cost Plus Method: Alternatively, the Cost Plus Method can be applied, where the fee is determined as the sum of the parent company's actually incurred costs and an appropriate profit mark-up. Here, the parent company would have to prove which costs were incurred for rendering the advisory service and how these costs were supplemented by a market-customary profit mark-up.

- Application in the case: To check the arm's length nature of the fee, a price comparison can be used, for example. For this, remunerations for comparable financing advice between independent companies are considered. If the paid fee is at arm's length, it can generally be recognised as a chargeable service.

- Distinction between Chargeable Services and "Shareholder Expenses":

- Principle: "Shareholder expenses" are expenditures incurred in the interest of the parent company or the overall corporate group and do not specifically serve the business operations of the subsidiary. Such expenditures are not tax-deductible.

- Application in the case: It must be checked whether the financing advice occurs exclusively in the interest of the German subsidiary or whether it also serves the parent company or the entire group. If the advice benefits the entire group, the fee could be classified as a "shareholder expense" and would thus not be deductible.

- Documentation Obligations according to § 90 Abs. 3 Abgabenordnung (AO):

- Principle: § 90 Abs. 3 AO obliges companies to document transfer prices to prove the appropriateness of the services and the fees paid for them.

- Application in the case: The German subsidiary must document the received advisory services and the fee paid for them in detail. This includes the explanation of the type of service, the business benefit, and the appropriateness of the remuneration. Without proper documentation, the tax authority might not recognise the business expense.

- § 4 Abs. 5 Nr. 7 Einkommensteuergesetz (EStG) – Non-deductible Business Expenses:

- Principle: According to § 4 Abs. 5 Nr. 7 EStG, expenditures for services attributable to the private sphere or the shareholder sphere are not deductible as business expenses.

- Application in the case: Should the financing advice be classified as a service that is rather attributable to the shareholder sphere (parent company), the fee for this service would not be tax-deductible.

Summary:

- Chargeable Service:

- The fee that the German subsidiary pays to the parent company for financing advice is recognised as a chargeable service if the service is in the interest of the subsidiary and is rendered at arm's length conditions.

- Deductibility as a Business Expense:

- If the advice is in the interest of the German subsidiary and the payment is at arm's length, the fee can be tax-deductible as a business expense. However, if the advice is classified as a "shareholder expense", the fee is not deductible.

- Documentation Obligations:

- To ensure deductibility, the German subsidiary must properly document the services rendered and the appropriateness of the fee.

- Risks:

- If the advice is classified as a "shareholder expense" or the documentation is insufficient, the tax authority might not recognise the business expense, which could lead to an additional tax burden.

Conclusion: The classification of services as chargeable and their deductibility as business expenses depends significantly on whether the service occurs in the interest of the subsidiary and is rendered at arm's length conditions. Careful documentation and a clear distinction from "shareholder expenses" are crucial to avoid tax risks.

**

Note

**This article serves as general information and was carefully prepared by the Lexo.Tax editorial team. Personal tax advice can only be provided within the framework of membership at Lexo.Tax – and exclusively to the extent permitted by law according to § 4 Nr. 11 StBerG (Tax Consultancy Act).