The Single Market and its Relevance (Art. 26 para. 2 TFEU)

The Single Market, created by the Maastricht Treaty and the Treaty on the Functioning of the European Union (TFEU), enabled an extensive economic integration of the member states of the European Union from 1993 onwards. Article 26 Paragraph 2 TFEU defines the Single Market as an area without internal frontiers (free movement without internal borders) in which the free movement of goods, persons, services and capital is ensured. This principle is central to the EU, as it aims to reduce trade barriers and promote closer economic integration.

For German corporations, the Single Market meant a significant expansion of their operational possibilities. The abolition of customs barriers and the harmonisation of regulations created a unified market with over 300 million consumers (at the time), which opened up enormous growth opportunities, particularly for export-oriented companies. The Single Market also promoted competition and forced companies to increase their efficiency and innovative strength in order to remain competitive in the now larger and more open market.

Art. 26 (ex-Article 14 TEC)

(1) The Union shall adopt measures with the aim of establishing or ensuring the functioning of the internal market, in accordance with the relevant provisions of the Treaties.

(2) The internal market shall comprise an area without internal frontiers in which the free movement of goods, persons, services and capital is ensured in accordance with the provisions of the Treaties.

(3) The Council, on a proposal from the Commission, shall define the guidelines and conditions necessary to ensure balanced progress in all the sectors concerned.

These four fundamental freedoms (which apply universally and generally) form the foundation of the Single Market and aim to reduce trade barriers and promote closer economic integration within the EU.

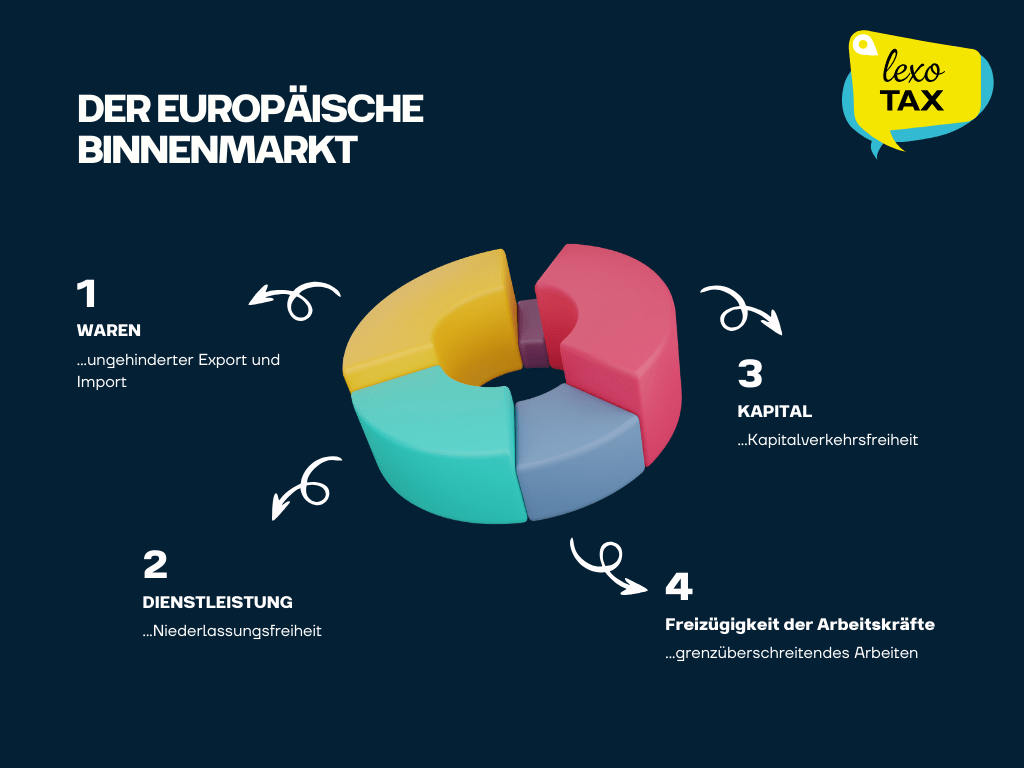

Four Fundamental Freedoms

- Free movement of goods: Enables the free exchange of goods between member states without the application of customs duties, quantitative restrictions or other trade barriers. Examples: Prohibition of import and export duties, abolition of all quantitative restrictions Art. 28 ff. TFEU

- Free movement of persons: Ensures the right of EU citizens to move freely within the member states, to work and to live there. Examples:

- Freedom of movement for workers Art. 45 ff. TFEU as well as the Schumacker ruling and

- Freedom of establishment Art. 49 ff. TFEU as well as the ECJ ruling Avoir fiscal and the Cadbury Schweppes case (C-196/04)

- Freedom to provide services: Guarantees that companies and individuals can offer and receive services in other member states without being hindered by discriminatory or disproportionate measures. This refers to the same services as in the case of freedom of establishment, but with a temporary character (does not require permanent establishment in the host state). Examples:

- Art. 56 ff. TFEU as well as C-294/97 Eurowings Luftverkehrs AG

- Freedom of capital movement: Refers to the free flow of capital and payments between member states as well as between the EU and third countries. In principle, all restrictions on the movement of capital (including monetary and material capital) between member states are prohibited. Examples:

Freedom of Capital Movement and Freedom of Establishment

The freedom of capital movement and freedom of establishment, which were established within the framework of the Single Market, played a key role in the restructuring and internationalisation of German corporations. Freedom of capital movement meant that investors could transfer capital to other EU member states and invest there without encountering obstacles. This led to an increasing dissolution of "Deutschland AG" – a system in which German companies were linked to one another through a network of mutual shareholdings and thus exhibited a strong domestic orientation.

The liberalisation of the capital market and the possibility for foreign investors to take stakes in German companies broke up national shareholding structures. This development was reinforced by the freedom of establishment, which enabled companies to found subsidiaries and permanent establishments in other EU countries and thus expand their market presence.

Particularity of the Freedom of Capital Movement

The freedom of capital movement holds a special position among the fundamental freedoms, as it applies not only within the EU but also towards third countries. This is established in Art. 63 TFEU, which guarantees the free movement of capital and payments between member states and between member states and third countries.

Special Features:

- Universal application: The freedom of capital movement is universally applicable and not limited to the EU Single Market. It also applies to capital movements between the EU and third countries, making it unique among the four fundamental freedoms.

- Comprehensive protection: It covers a wide range of transactions, including direct investments, real estate purchases, securities transactions and banking operations. This ensures that capital in any form can be moved without restrictions between member states and third countries.

- Judicial enforceability: Like the other fundamental freedoms, the freedom of capital movement is judicially enforceable. Affected parties can invoke the freedom of capital movement before national courts or the European Court of Justice (ECJ) to take action against restrictions.

- Limited justification possibilities: Restrictions on the freedom of capital movement are only permissible under narrow conditions, e.g. for reasons of public policy or public security. Furthermore, such restrictions must be proportionate.

Challenges in the Area of Direct Taxes

Art. 26 para. 2 TFEU and Art. 115 TFEU play a decisive role in the area of direct taxes within the European Union, even though the EU has no explicit legislative competence in this area of direct taxation.

Challenge: Different national tax systems, particularly in the area of direct taxes, can hinder the idea of a free Single Market. This is in contradiction to the objective of a unified Single Market anchored in Art. 26 para. 2 TFEU. Freedoms collide with the boundaries of 27 different tax systems.

The ECJ states the following in this regard: "Although direct taxation falls within their competence, the Member States must none the less exercise that competence consistently with Community law." Consequence: Primacy of EU law over national law. This does not mean, however, that national norms are invalid; rather, the facts that violate EU law simply cannot be applied (validity-preserving reduction).

Art. 115 TFEU (ex-Article 94 TEC)

Without prejudice to Article 114, the Council shall, acting unanimously in accordance with a special legislative procedure and after consulting the European Parliament and the Economic and Social Committee, issue directives for the approximation of such laws, regulations or administrative provisions of the Member States as directly affect the establishment or functioning of the internal market.

- Significance: Since the EU has no explicit legislative competence in the area of direct taxes, Art. 115 TFEU serves as the central legal basis for adopting tax measures to ensure the Single Market. This article enables the EU to issue directives that harmonise national tax regulations, provided this is necessary for the functioning of the Single Market.

- Requirements and Restrictions:

- Unanimity in the Council, which makes the adoption of such directives difficult, as the interests of the member states often diverge significantly. Furthermore, this is tied to other strict requirements.

- Not every tax measure can be harmonised. Harmonisation is only permissible if it is necessary to eliminate obstacles to the free movement of goods, persons, services and capital or to prevent distortions of competition within the Single Market. There is thus a limited application for harmonisation under Art. 115 TFEU.

- Furthermore, measures must also respect the subsidiarity principle. This means that the EU may only act if the targeted objectives cannot be sufficiently achieved at national level and an EU-wide regulation is therefore necessary.

- The measures must also be proportionate, meaning they must not go beyond what is necessary to achieve the Single Market objectives.

- Dilemma: The need for harmonisation to make the Single Market functional stands in conflict with the difficulty of achieving unanimity in the Council. Each member state defends its tax policy interests, which makes the implementation of harmonising measures in the area of direct taxes challenging.

Art. 26 para. 2 TFEU and Art. 115 TFEU are of central importance for the area of direct taxes because they are intended to guarantee the free Single Market on the one hand, while on the other hand providing the possibility to eliminate tax differences that could harm the Single Market via harmonising directives. However, the practical implementation of such measures is very challenging due to the required unanimity in the Council.

Single Market Tax Directives

The Single Market tax directives, consisting of the Merger Directive, the Parent-Subsidiary Directive, and the Interest and Royalties Directive, had profound effects on the cross-border activities of companies within the EU.

Merger Directive (90/434/EEC / 2009/133/EC): This directive eliminated the tax barriers that previously existed for company mergers, particularly the risk of disclosing hidden reserves. Before 1993, a cross-border restructuring was often associated with significant tax burdens, as hidden reserves had to be disclosed and taxed immediately. The Merger Directive provided relief for the restructuring of companies within the EU by enabling tax neutrality for mergers, divisions, transfers and conversions. This promoted the formation of large European corporations and the creation of so-called EU champions that were competitive on the global market. You can find more information here:

Parent-Subsidiary Directive (90/435/EEC / 2011/96/EU): This directive eliminated the double taxation of dividends between parent and subsidiary companies in different EU countries. Previously, dividends were frequently taxed both in the state of the subsidiary and in the state of the parent company. The directive led to an exemption from withholding tax on dividends and thus prevented double taxation. This facilitated the formation of cross-border corporate structures and allowed capital to be allocated more efficiently within a group. You can find more information here:

Interest and Royalties Directive (2003/49/EC): This directive abolished the double taxation of interest and royalty payments between associated companies in different EU states. Before the introduction of this directive, interest and royalty payments often led to tax deductions in the country of the payer and simultaneous taxation in the country of the recipient, which complicated international business activities. The directive enabled companies to make such payments without the deduction of withholding taxes, which increased the liquidity and profitability of international business. You can find more information here:

Impact on German Corporations

The implementation of these directives led to the breaking up of traditional national shareholding structures and enabled German corporations to expand their international activities without the previously existing tax barriers. The freedom of capital movement and the freedom of establishment, which were strengthened by the Single Market, enabled new investors to take stakes in German companies more easily and promoted the internationalisation of German companies.

Through the harmonisation of the tax framework and the elimination of double taxation, German corporations were able to design their structures more efficiently and compete better with other international companies. The tax advantages of the directives thus contributed significantly to the internationalisation as well as the development of large German corporations and the creation of a competitive European Single Market.

Note: This article serves for general information purposes and was carefully prepared by the editorial team of lexo.tax. Personal tax advice can only be provided within the framework of a membership with lexo.tax – and exclusively to the extent legally permitted according to § 4 Nr. 11 StBerG (Tax Consultancy Act).